Vacation Home or Rental Property in BC: The Tax Implications to Know

Buying a vacation home or rental property in British Columbia can feel like a smart lifestyle and investment decision. You may want a family getaway, a future retirement property, a short-term rental, or a long-term income property.

But before you buy, rent, or sell, it is important to understand the tax side.

A second property is not treated the same way as your principal residence. Rental income may need to be reported. Expenses may be deductible, but not always in full. Short-term rentals can trigger additional GST, PST, and local accommodation taxes. And when the property is eventually sold, capital gains tax may apply.

This article breaks down the key tax considerations for BC vacation homes and rental properties in plain language.

A Vacation Home Is Usually Not Fully Tax-Free When Sold

In Canada, your principal residence may qualify for the principal residence exemption. If a property was your principal residence for every year you owned it, you may not have to pay tax on the gain when it is sold. However, a vacation home, cabin, cottage, or second property usually does not receive the same full exemption unless it is designated as your principal residence for specific years.

This matters because families sometimes assume that a second home can be sold tax-free like their main home. In many cases, it cannot.

For example, if you bought a BC vacation property for $600,000 and later sold it for $900,000, the $300,000 increase may create a taxable capital gain unless the principal residence exemption applies to some or all of the ownership period.

The planning question becomes: which property should be designated as your principal residence for which years? That decision can affect your future tax bill, especially if both properties have increased in value.

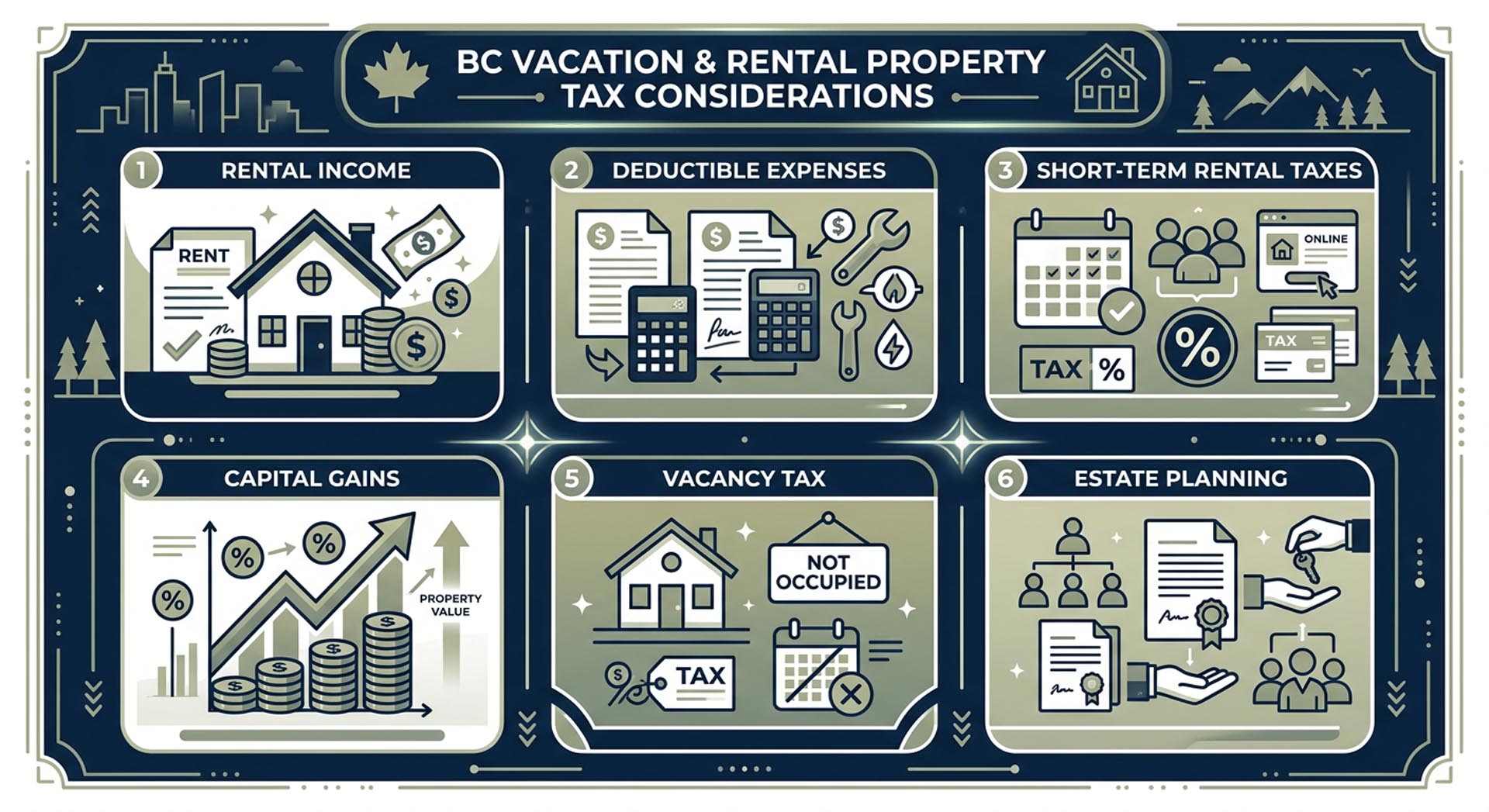

Rental Income Must Be Reported

If you rent out your vacation home or rental property, the income generally needs to be reported on your tax return. CRA’s rental income guide explains how rental income, deductible expenses, and net rental income or loss are reported, including through Form T776, Statement of Real Estate Rentals.

This applies whether the property is rented long-term to tenants or rented occasionally as a vacation rental.

Common examples of rental income include:

- Monthly rent from a tenant

- Short-term rental income from platforms like Airbnb or Vrbo

- Seasonal rental income

- Fees charged for parking, cleaning, or extra guests

Even if the property is only rented for part of the year, that income may still need to be reported.

Some Expenses May Be Deductible

Rental property owners can generally deduct reasonable expenses incurred to earn rental income. CRA separates expenses into current expenses and capital expenses. Current expenses may include ordinary operating costs, while capital expenses usually improve the property or provide a longer-term benefit.

Possible deductible expenses may include:

- Mortgage interest, not principal repayment

- Property taxes

- Insurance

- Utilities

- Repairs and maintenance

- Condo or strata fees

- Advertising

- Professional fees

- Property management fees

- Cleaning fees

- Some travel costs directly related to managing the rental

The key phrase is “to earn rental income.” If the property is used personally and rented out part-time, expenses usually need to be split between personal use and rental use.

For example, if you use the property personally for part of the year and rent it for part of the year, you generally cannot deduct 100% of the annual costs against rental income.

Personal Use Can Complicate the Tax Treatment

Many BC vacation homes are mixed-use properties. The owner might use the property for family weekends, holidays, or summer stays, while also renting it out during other periods.

This creates a tax issue because the property is partly personal and partly income-producing.

A simple example:

You own a vacation condo in Kelowna. You personally use it for 60 days of the year and rent it for 120 days. You may need to allocate certain expenses based on rental use versus personal use.

This is one of the reasons recordkeeping matters. Owners should track:

- Dates rented

- Dates used personally

- Rental income collected

- Cleaning and maintenance expenses

- Repairs

- Mortgage interest

- Property taxes

- Insurance

- Platform fees

- Professional fees

Good records make tax filing easier and reduce the risk of guessing later.

Short-Term Rentals Have Additional Tax Rules

Short-term rentals can create more tax complexity than long-term rentals.

CRA has introduced rules that can deny certain deductions for non-compliant short-term rentals after 2023. A short-term rental generally refers to a residential property rented or offered for rent for less than 90 consecutive days.

This means compliance matters. If the rental is not permitted under provincial, municipal, or local rules, the owner may lose the ability to deduct some expenses related to that short-term rental income.

In BC, short-term accommodation can also be subject to provincial sales tax. The Province of BC states that 8% PST applies to short-term accommodation in BC unless a specific exemption applies. In participating areas, the Municipal and Regional District Tax, or MRDT, can also apply, generally up to 3%.

GST may also become an issue. Short-term accommodation is generally taxable for GST purposes, and registration may be required if the host exceeds the $30,000 small supplier threshold.

For owners, the takeaway is simple: a short-term rental is not just “extra income.” It may come with registration, collection, remittance, and compliance responsibilities.

BC’s Speculation and Vacancy Tax May Apply

Some BC residential properties are subject to the Speculation and Vacancy Tax. This tax is designed to target vacant homes in certain regions of the province. Owners may need to complete an annual declaration and may owe tax if they do not qualify for an exemption. For 2026, the Province of BC lists the speculation and vacancy tax payment due date as July 2, 2026.

This is especially important for second homes, vacation properties, and properties that are not rented long enough to qualify for an exemption.

The rules depend on location, occupancy, ownership type, and use of the property. A vacation home that sits empty for much of the year could create a very different tax result than a property used as a principal residence or rented to a long-term tenant.

Capital Cost Allowance Should Be Used Carefully

Rental property owners sometimes ask whether they should claim depreciation, known as Capital Cost Allowance or CCA.

CCA can reduce taxable rental income in the short term. However, it can create problems later. If the property is sold for more than its depreciated value, some of the CCA previously claimed may be brought back into income as recapture.

There is also a planning issue if the property may later become a principal residence or if the owner wants to preserve flexibility around the principal residence exemption.

This does not mean CCA is always bad. It means it should be reviewed carefully before claiming it.

Selling the Property Can Trigger Capital Gains Tax

When a vacation home or rental property is sold, the owner may have to report a capital gain. The basic calculation is:

Selling price minus adjusted cost base minus selling costs equals capital gain.

The adjusted cost base may include the original purchase price plus certain costs, such as legal fees, land transfer tax, and eligible capital improvements.

Selling costs may include realtor commissions, legal fees, and other costs related to the sale.

The federal government announced in 2025 that the proposed increase to the capital gains inclusion rate would be cancelled. Still, capital gains rules are a moving area of tax planning, so owners should confirm the current treatment before selling.

For higher-value BC properties, even a modest percentage increase in value can create a major taxable gain.

Estate Planning Matters Too

Vacation homes often become emotional family assets. Parents may want to leave the property to children. Siblings may want to share ownership. One child may want to keep the property while another wants to sell.

From a tax perspective, this can become complicated.

A transfer during life, a transfer at death, or a sale to family may trigger tax consequences. The property may also create liquidity problems if the estate owes tax but does not have enough cash available.

This is why vacation properties should be part of estate planning, not just income tax planning.

Important questions include:

- Who will own the property later?

- Will the family keep it or sell it?

- Will there be enough cash to pay tax?

- Should insurance be used to cover tax exposure?

- Should ownership be individual, joint, corporate, or trust-based?

- How will family members handle expenses and usage rights?

The earlier these questions are discussed, the easier it is to avoid conflict.

Before Buying a BC Vacation or Rental Property, Build a Tax Plan

A vacation home or rental property can be a valuable asset, but the tax rules should be reviewed before major decisions are made.

Before buying, renting, converting, or selling, consider these planning questions:

- Will the property be personal use, rental use, or both?

- Will it be rented short-term or long-term?

- Is the property located in an area affected by BC’s speculation and vacancy tax?

- Will PST, MRDT, or GST apply?

- How will expenses be tracked and allocated?

- Could the property qualify for the principal residence exemption for any years?

- What happens if the property is sold?

- What happens if the property is passed to family?

The best time to think about tax is before the transaction, not after.

Final Thought

A BC vacation home or rental property can support lifestyle, income, and long-term wealth planning. But it can also create tax obligations that are easy to overlook.

Rental income, short-term rental compliance, GST, PST, MRDT, vacancy taxes, capital gains, and estate planning can all affect the true return on the property.

Before making a decision, speak with a qualified tax advisor or financial planner who understands your full situation.

Schwartzman Financial Group helps Canadians think through tax, insurance, and wealth planning decisions with clarity. If you own or are considering a vacation home or rental property in BC, now is the time to understand the tax picture before it becomes expensive.