Tips for Business Owners Taking Time Off: A Succession Planning Reminder

For many business owners, taking time off sounds simple in theory.

Step away.

Recharge.

Spend time with family.

Travel.

Disconnect for a few days.

But in reality, many owners find it difficult to leave the business, even briefly.

They worry about clients, staff, payroll, cash flow, operations, emergencies, and decisions that usually run through them.

If the business cannot function without the owner for a week or two, that is not just a vacation problem.

It may be a succession planning problem.

Taking time off can reveal how dependent the business is on one person. It can also show where better systems, leadership, documentation, insurance, and long-term planning may be needed.

This article breaks down practical tips for business owners preparing to take time away, and why those same steps can support a stronger succession plan.

Time Off Is a Test of Business Continuity

A business owner’s vacation can act like a small stress test.

If every client question, staff issue, payment approval, supplier decision, or operational problem depends on the owner, the business may be carrying too much key-person risk.

That does not mean the owner has done something wrong. In many small and mid-sized businesses, the owner is deeply involved because they built the company from the ground up.

But over time, the business should become less dependent on one person.

A strong business continuity plan helps the company keep operating during temporary disruptions. That may include vacations, illness, family emergencies, leadership changes, or unexpected events.

Before taking time off, ask:

- Can the business operate without me for one week?

- Who can make decisions while I am away?

- Who has access to critical information?

- Are client expectations clear?

- Are payment approvals covered?

- Can staff handle common issues?

- What happens if there is an emergency?

If these questions create stress, the business may need a stronger continuity plan.

Decide What Truly Requires the Owner

Many owners are involved in everything.

Sales. Operations. Hiring. Client relationships. Approvals. Finances. Problem solving. Strategy.

But not every decision requires the owner.

A useful exercise is to list the decisions that happen in the business each week and divide them into three categories:

Owner-only decisions

These are major decisions that should still wait for the owner, such as large financial commitments, major hiring decisions, legal issues, major client escalations, or strategic changes.

Delegated decisions

These are decisions trusted team members can make while the owner is away, such as scheduling, routine client communication, standard purchases, and day-to-day operations.

System-based decisions

These are issues that should not require a person at all because they can be handled through documented processes, checklists, templates, or software.

The more decisions that can move out of the “owner-only” category, the more resilient the business becomes.

This is also an early step toward succession planning.

If no one else can make decisions, no one else can eventually lead.

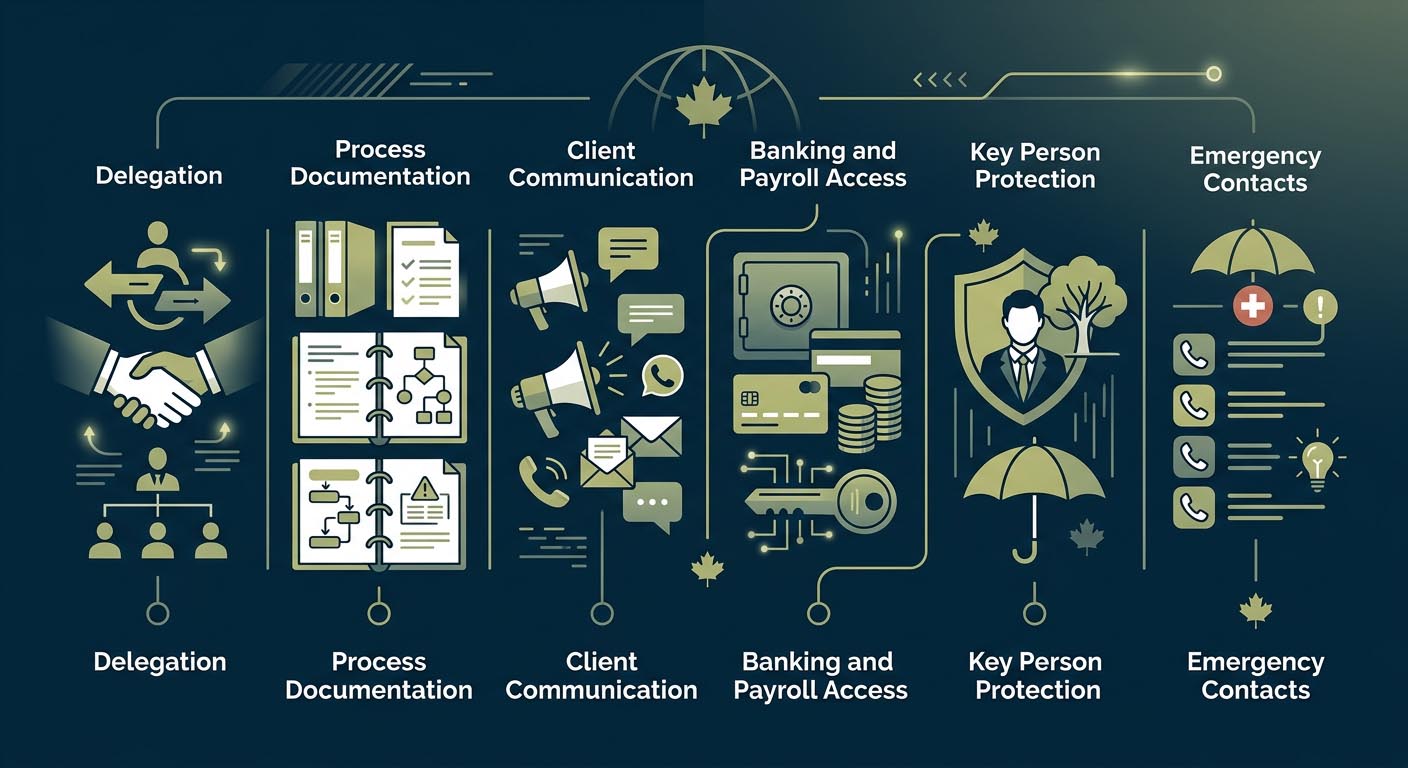

Build a Clear Delegation Plan

Delegation is not just telling someone, “You are in charge while I am gone.”

A strong delegation plan should define:

- Who is responsible for what

- What decisions they can make

- What spending limits apply

- Which clients or projects need special attention

- When to escalate an issue

- How updates should be shared

- What can wait until the owner returns

This should be written down.

Clear delegation reduces confusion and helps team members feel more confident. It also helps the owner actually step away instead of checking in constantly.

For a short vacation, this may be simple.

For long-term succession, the same principle applies on a larger scale.

The business needs capable people who understand their responsibilities, authority, and limits.

Document the Core Processes

Many businesses rely on knowledge that lives inside the owner’s head.

That can become a major risk.

If the owner is away, unavailable, sick, or preparing to exit, undocumented knowledge can create operational bottlenecks.

Start with the processes that matter most:

- How new clients are handled

- How estimates or proposals are prepared

- How invoices are approved

- How payroll is managed

- How supplier orders are placed

- How customer complaints are escalated

- How sales opportunities are tracked

- How key software is used

- How banking and payment approvals work

- How staff schedules are managed

The goal is not to create a massive manual overnight.

The goal is to slowly remove dependency from one person.

A good starting point is to document the tasks that only the owner knows how to do.

Create an Emergency Contact and Decision Tree

Before taking time off, business owners should create a simple emergency plan.

This does not need to be complicated.

It should answer:

- Who is the first point of contact?

- Who handles client issues?

- Who handles staff issues?

- Who handles banking or payment problems?

- Who contacts the accountant, lawyer, or advisor if needed?

- What counts as an emergency?

- What can wait until the owner returns?

A decision tree can help.

For example:

If the issue is under a certain dollar amount, the manager can approve it.

If the issue involves a key client, contact the assigned lead.

If the issue is legal, contact the lawyer.

If the issue is tax-related, contact the accountant.

If the issue is urgent and outside normal authority, contact the owner.

This protects both the owner and the team.

It also reveals whether the business has the right advisory support in place.

Review Banking, Payroll, and Signing Authority

Many business owners are the only person who can approve payments, sign documents, move money, or handle payroll.

That may work day to day, but it can become a problem when the owner is away.

Before taking time off, review:

- Who can approve payroll?

- Who can pay suppliers?

- Who can access banking records?

- Who can sign cheques or authorize transfers?

- Who can manage tax installment deadlines?

- Who can approve urgent expenses?

- What controls are in place to prevent misuse?

This does not mean giving full access to everyone.

It means setting up responsible backup authority with clear controls.

From a succession planning perspective, financial authority is one of the most important areas to handle carefully.

A future transition is harder if no one else understands the financial operations of the business.

Protect Key Client Relationships

In many owner-led businesses, clients are loyal to the owner personally.

That can be a strength, but it can also create risk.

If clients only trust one person, the business may be harder to scale, sell, or transfer.

Before taking time off, introduce clients to the person who will support them while the owner is away.

This can be done through a simple email:

“I will be away from July 10 to July 17. During that time, Sarah will be your main point of contact for anything urgent. She is fully briefed and will be able to help.”

This does two things.

It reassures the client.

It strengthens the client’s relationship with the broader business.

Over time, this helps move value from the owner personally into the business itself.

That matters for succession planning and business valuation.

Use Time Off to Identify Leadership Potential

When the owner steps back, other people have a chance to step forward.

This can be valuable.

A short period away may reveal:

- Who takes initiative

- Who communicates clearly

- Who handles pressure well

- Who needs more training

- Who clients trust

- Who understands the business beyond their job description

- Who may be a future leader

Succession planning is not only about choosing a future owner.

It is also about developing the people who can keep the business strong.

Sometimes the best way to identify leadership potential is to give people space to lead.

Review Key Person Risk

If the business depends heavily on the owner, the business may have key person risk.

Key person risk means the company could suffer significant financial or operational disruption if a critical person becomes unavailable.

That person might be the owner, a top salesperson, a technical expert, an operations manager, or someone who holds important client relationships.

Business owners should ask:

- What would happen if I could not work for 30 days?

- What would happen if I could not work for six months?

- What would happen if a key employee left suddenly?

- Would revenue continue?

- Would clients stay?

- Would staff know what to do?

- Would the business have enough cash?

- Would insurance help?

Key person insurance, disability protection, buy-sell funding, and business continuity planning can all play a role.

The right solution depends on the business structure, ownership, revenue model, and long-term goals.

Insurance Can Support Business Continuity

Insurance is often overlooked in succession planning, but it can be important.

Depending on the situation, business owners may need to review:

- Life insurance

- Disability insurance

- Critical illness insurance

- Key person insurance

- Buy-sell agreement funding

- Corporate-owned insurance

- Business overhead expense insurance

Insurance can help create liquidity when the business needs cash.

That may include funding a buyout, protecting family income, covering business expenses, replacing a key person, supporting debt repayment, or giving the business time to adjust during a transition.

Insurance does not replace operational planning.

But it can support the plan when something unexpected happens.

Time Off Can Reveal Whether the Business Is Saleable

Many owners eventually want to sell their business or transition it to family, employees, or another buyer.

But buyers usually want a business that can operate without the owner being involved in every detail.

If the business depends completely on the owner, it may be harder to transfer.

A more saleable business often has:

- Documented systems

- Reliable financial records

- Strong management

- Recurring revenue

- Clear client relationships

- Lower owner dependency

- Consistent cash flow

- Defined roles and responsibilities

- Transferable processes

- Clean legal and tax structure

Taking time off is one simple way to test whether the business has these qualities.

If the business struggles while the owner is away, that is useful information.

It shows what needs to improve before a future sale or transition.

Succession Planning Is Not Only About Retirement

Many business owners think succession planning means planning for retirement.

It can.

But succession planning is broader than that.

It also applies to:

- Vacations

- Health events

- Family emergencies

- Temporary leave

- Business growth

- Leadership development

- Partner exits

- Unexpected death or disability

- Sale of the business

- Family business transition

- Management buyout

- Intergenerational wealth planning

Succession planning is really about continuity.

Who can lead?

Who can decide?

Who can protect the value of the business?

Who can carry the business forward if the owner steps back?

Those questions matter whether the owner is gone for two weeks or planning an exit over five years.

A Practical Checklist Before Taking Time Off

Before stepping away, business owners should review:

- Who is in charge while I am away?

- Who can make operational decisions?

- Who can approve expenses?

- Who can handle payroll or supplier payments?

- Are clients aware of the temporary point of contact?

- Are staff responsibilities clear?

- Are key processes documented?

- Are passwords and access handled securely?

- Are emergency contacts listed?

- Are tax, payroll, or filing deadlines covered?

- Is the business protected if something unexpected happens?

- What did this process reveal about our succession plan?

This checklist is simple, but it can highlight important gaps.

After Returning, Review What Happened

The most important succession planning work may happen after the owner returns.

Ask the team:

- What worked well?

- What problems came up?

- What decisions were unclear?

- What information was missing?

- Where did clients need reassurance?

- What tasks still depended on the owner?

- Who stepped up?

- What needs to be documented?

- What should be delegated permanently?

This turns time off into a business improvement exercise.

Each vacation, absence, or break can make the business stronger if the lessons are captured.

Final Thought

Taking time off should not feel impossible.

If it does, the business may be too dependent on the owner.

That is not just a lifestyle issue. It is a succession planning issue.

A business that can operate without the owner for a short period is often more resilient, more valuable, and better prepared for the future.

Strong succession planning is not only about who takes over one day.

It is about building systems, leadership, protection, and clarity today.

Schwartzman Financial Group helps business owners think through succession planning, insurance, tax planning, wealth management, and long-term financial strategy.

Because eventually, every owner steps away.

The question is whether the business is ready.

Commonly Asked Questions

Why is taking time off important for business owners?

Taking time off helps business owners recharge, but it also tests whether the business can operate without them. If the company struggles during a short absence, it may reveal gaps in delegation, documentation, leadership, or succession planning.

What is succession planning for business owners?

Succession planning is the process of preparing the business to continue operating when the owner steps back, exits, retires, becomes unavailable, or transfers ownership. It may involve leadership development, tax planning, insurance, business valuation, legal agreements, and continuity planning.

How can a business owner prepare for vacation?

A business owner can prepare by delegating authority, documenting key processes, setting emergency contacts, reviewing banking and payroll access, notifying key clients, and creating a clear decision-making plan for staff.

What is key person risk?

Key person risk happens when a business depends heavily on one owner, employee, or leader. If that person becomes unavailable, the business may face revenue loss, operational disruption, client issues, or financial pressure.

How does insurance support succession planning?

Insurance can provide liquidity if an owner, partner, or key person dies, becomes disabled, or is unable to work. It may help fund a buyout, cover business expenses, protect family income, or give the business time to transition.

Does succession planning only apply to retirement?

No. Succession planning also applies to temporary absences, illness, family emergencies, partner exits, business sales, ownership transitions, and unexpected events. It is about business continuity, not just retirement.

What should business owners review after returning from time off?

They should review what worked, what failed, which decisions were unclear, which processes were missing, who stepped up, and what should be improved before the next absence or future transition.